Do you know what is Input Tax Credit (ITC)?

Input Tax Credit (ITC) is one of the important features of GST. The buyer has to pay tax in the purchase of a flat or apartment. Let us know about it in detail about GST on Real Estate.

Input Tax Credit

Input Tax Credit (ITC) is a process where the suppliers of goods or services can reduce their tax burden by receiving a tax credit on inputs used to manufacture the goods or services. For example, If a jeweller contracts a third party (job worker) to design a particular piece of jewellery and pays GST on the amount charged by the job worker. The tax paid is adjusted with the total GST due at the time final sale to the customer. This Input Tax Credit amount is not paid out in cash but instead credited to the electronic credit ledger of the GST registered business/individual. So, ITC in GST is the ideal mechanism to prevent the effect of tax effect under the VAT.

Input Tax Credit in Real Estate Sector

In the real estate sector, construction of a residential project includes a GST component for many stakeholders and promoters. They include architects, contractors, and raw material suppliers. The promoter makes the payments for suppliers like cement and sand as well as services such as building plan/design creation which includes GST rates. In the new proposed budget 2019, GST is charged as an ITC by the promoter of the particular project, which reduces the burden of tax payments.

Goods and Services Tax (GST) came into force on July 1, 2017. The GST is charged on the supply of goods and services.

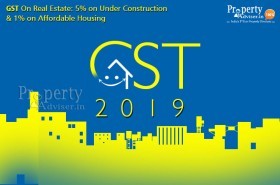

In the recent budget 2019, the input tax credit was removed in case of residential real estate transactions. The new proposed GST rates for residential under construction properties are 1% GST for affordable housing transactions previous it was 8%. The properties which are not under affordable housing scheme 5% GST is applicable and previous it was 12%.

What are the Advantages of New GST Rates for Real Estate Sector?

The proposed benefits of decreased GST rates in real estate to be implemented from 1st April 2019.

- The price of the house will decrease especially in the affordable housing segment.

- Resolution of problems about ITC benefits not to be passed on to buyers.

- Elimination of problems related to unused ITC which is added to the cost of the property.

- Simple tax structure as well as compliance for builders.

GST Rates in Real Estate Sector

One Time Option on Under Construction Projects

For ongoing projects where construction and actual booking have both started before 1 April 2019 and which are not completed by 31 March 2019, developers would be given a one-time option to pay tax at the old rates, i.e. 8% or 12%with ITC. This option is applicable within the prescribed time if not the new rates would apply.

One Percent Tax Without ITC

- 1% Tax without input tax credit (ITC) is applicable for all the affordable houses which were constructed in an area 60 sq.mt in non- metros and 90 sq.mt in metros. Also, the value of the property should be up to RS. 45 lakhs

- The ongoing affordable housing constructing by the existing central and state housing schemes are presently eligible for an allowed rate of 8% GST.

Five Percent Tax without the Input Tax Credit

- If you booked the under construction house before or after 1st Apr 2019, then 5% of GST without ITC shall be applicable to this. You can pay the taxes on an installment basis on or after Apr 2019.

- All the properties which are not affordable.

- Commercial properties such as shops, offices etc. in a residential real estate project (RREP) in which the carpet area does not exclude more than 15%.

Conditions of the New Tax Rates

The new tax rates of 1% tax is applicable for the construction of affordable houses and 5% on other than affordable homes will be applied based on the following conditions.

- The input tax credit is not available.

- 80% of inputs and input services shall be purchased from registered persons except for capital goods, TDR/ JDA, FSI, long term lease premiums.

- On shortfall of purchases from registered persons, the 18 % tax shall be paid by the builder on RCM basis.

- Also the purchase of cement from the unregistered person then the builder has to pay 28% tax under RCM and on capital goods at applicable rates.

ITC rules are introduced to bring clarity on the monthly and final determination of ITC and reversal in real estate projects. The change would provide a procedure for availing input tax credit about commercial units would continue to eligible for an input tax credit in a mixed project.

Visit Property Adviser, the first real estate property directory portal to know trending residential properties for sale in Hyderabad. We furnish you detailed and verified information of independent houses, villas and apartments for sale in Hyderabad. It helps you to make wise decisions. Pave the smart way to buy your dream home and lead a happy life.

By: Shailaja K